How insurance needs change as your relationships change

Lifestyle

Audio By Carbonatix

4:45 PM on Thursday, February 12

By Susan Meyer for TheZebra, Stacker

How insurance needs change as your relationships change

With Valentine’s Day upon us and spring right around the corner, love and romance are top of mind for many. But the truth is that any time of year is appropriate to think about your connection with a significant other, especially when it comes to insurance matters. Because just as relationships evolve throughout your life, so can coverage needs.

“As you and your partner move through life, your financial responsibilities, shared property, and risk profiles can change,” the Insurance Information Institute’s Janet Ruiz tells TheZebra.com. “Updating insurance ensures that coverage accurately reflects these shifts and prevents unexpected gaps.”

Truth is, most Americans eventually partner up under a single roof, which means they’ll need to carefully navigate insurance matters. Consider that most adults younger than age 45 (59%) have cohabitated with an unmarried partner at some point, according to Pew Research, and married couples comprise nearly half (47%) of American households today, per the U.S. Census Bureau.

Let’s take a closer look at common relationship stages and how your homeowners/renters and car insurance requirements can change accordingly.

Moving in Together

Whether you plan to rent or own a home with an unmarried partner, give careful thought to renters or homeowners insurance, as well as auto coverage. The proper amount can provide valuable monetary support if your home or car is damaged by a covered peril. But you have to be aware of coverage deficiencies that many don’t expect.

“Some insurance gaps can show quickly when you live together,” says Beth Swanson, insurance analyst for The Zebra. “When only one partner is the legal homeowner, the other partner’s personal belongings often aren’t fully covered under the homeowner’s policy, making renters insurance necessary. Liability coverage is another common surprise, especially if both people share responsibility for the home, pets, or guests.”

Another overlooked aspect is whether your partner regularly drives your vehicle but isn’t listed on your auto policy. In this instance, you could have zero coverage if that partner causes an accident, as insurance companies can deny claims for undisclosed household drivers.

“Carriers generally define a household as people who live together at the same primary residence, regardless of marital status. This affects who must be listed on an auto policy and whose belongings are covered under a home or renters policy,” adds Ruiz.

Bundling auto and renters policies while unmarried can save you 5%, on average, per The Zebra. But keeping separate policies is advised in some scenarios, such as if you own separate vehicles, have different insurance histories, or aren’t ready to combine coverage yet.

Getting Married

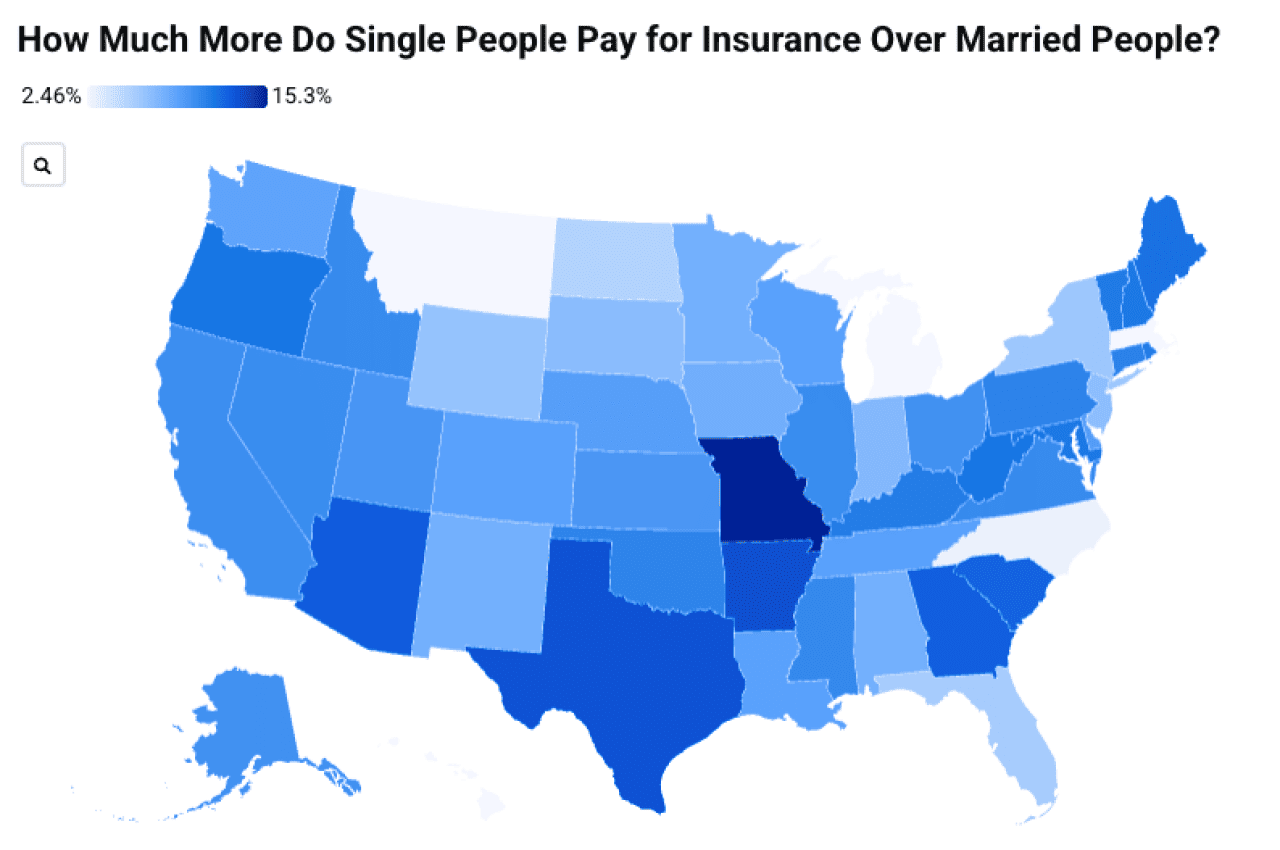

After you tie the knot, you can benefit from coordinated coverage, merged vs. separate policies and various discounts. Case in point: Married policyholders pay nearly 9% less, on average, for auto insurance than single drivers.

That difference isn't uniform around the country, though. In this map, you can see how much of a difference where you live makes in terms of how much less you pay (on average) as a married person.

But note that premiums depend on many factors, and combining policies isn’t always cheaper if one spouse has a higher rate or different coverage needs. Some couples maintain separate policies initially after marriage, particularly if they are keeping separate residences temporarily or have complex asset situations.

Personal finance expert Andrew Lokenauth says it’s wise to immediately review your insurance policies after getting married to add a spouse as an additional or named insured on policies and to add beneficiaries. Your focus at this stage should also be on improving protection, not just saving money. Smart early steps include raising liability limits and evaluating whether an umbrella policy is appropriate.

“You should also carefully review coverage limits and revise your deductibles to match combined finances,” notes Lokenauth. “I’ve seen couples wait months before addressing whether their $250,000 liability coverage adequately protects their now-combined $800,000 net worth, which is backwards thinking.”

If children enter the picture, revisit your coverage levels again and ensure that you have adequate protection in place for all your assets. Now’s a good time to think about adding life insurance, as well.

Separating or Divorcing

Unfortunately, plenty of relationships don’t work out. If you and your partner split up, you’ll want to properly review insurance policies to reflect changes in residence, vehicle ownership and financial responsibility.

“Both partners need clarity on who is covered, who will pay premiums, and how liability will be managed during the transition,” Ruiz says.

Insurance policies often remain shared longer than you’d expect during a separation. Living arrangements can quickly change, but the legal details and paperwork around homes, vehicles and ownership can require time to untangle, as divorce often takes months or years to finalize.

“These delays can create coverage and liability risks. For example, if both names are still on an auto or homeowners policy, one person’s accident, missed payment, or claim could still affect the other,” cautions Swanson.

Names should typically be removed from policies and paperwork once financial and ownership responsibilities have been legally divided, to prevent unwanted liability or exposure in the event of a claim.

Death of a Partner or Spouse

If your partner passes away, insurance and financial paperwork are often the last thing you want to think about. In the short term, most policies remain active, but you’ll likely need to update them once you are ready.

“Insurance companies may need to adjust your policy based on who is now listed as the primary insured, who owns the home or vehicles, and whether the household is changing,” says Swanson. “It’s a good idea to contact your carrier when you can, to make sure coverage continues smoothly, and there aren’t any unexpected gaps. You will also likely need a death certificate before you can change many of these financial loose ends.”

Be aware that many insurance discounts can disappear after a spouse’s death. Data from The Zebra indicate that widowed drivers pay an average of 3% more than married drivers but 5% less than single or divorced drivers.

“Household-based pricing that assumed two adults now reflects one, which can cause your premiums to jump 10% or more, even though your actual risk hasn’t changed,” says Lokenauth.

Considerations When It Comes to Insurance and Relationships

Fact is, life is dynamic, especially when two people are involved—which is why you shouldn’t view insurance as static. Insurance is built around households, ownership, and risk, all of which change over time.

“Major life transitions are a natural time to review all insurance policies, confirm accurate information, and update coverage to match new circumstances,” says Ruiz.

This story was produced by TheZebra and reviewed and distributed by Stacker.